Florida financial institutions and service providers are facing a stricter compliance environment than ever before. Federal Regulation F rules have expanded the ways debt collectors can contact consumers, and Florida's own Consumer Collection Practices Act layers additional requirements on top. If your business handles debt collection, including utility collections Florida, staying current on both sets of rules isn't optional.

Ready to protect your business now? Contact HF Holdings Inc. at (877) 680-6064 for a free consultation.

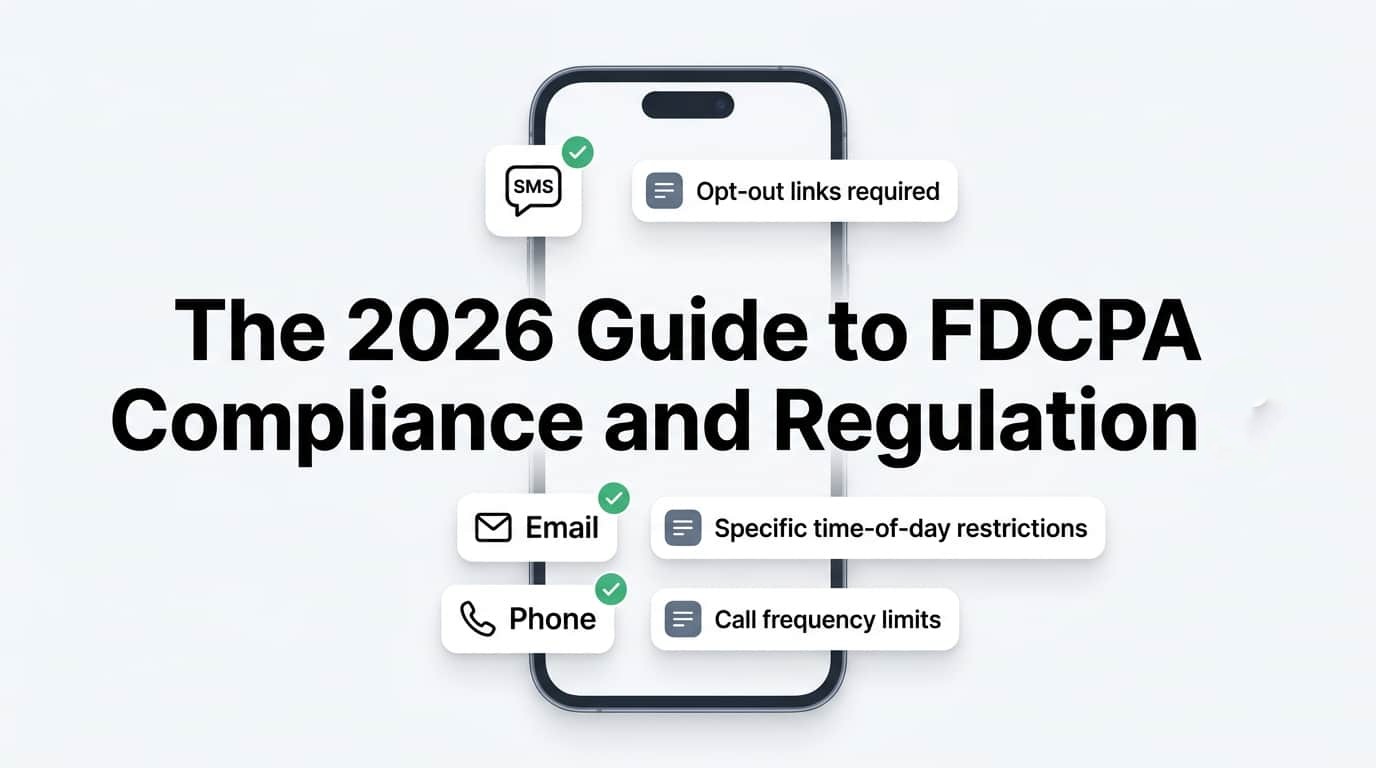

What Is Regulation F and How Does It Change FDCPA Rules?

Regulation F is the CFPB's formal rule implementing the Fair Debt Collection Practices Act (FDCPA). It took effect in November 2021 and set specific limits on how debt collectors communicate with consumers. Under Regulation F, collectors are capped at 7 phone call attempts per week per debt, and no more than 1 conversation within any 7-day period. Collectors can also use email and text messages to contact consumers, provided they follow strict opt-out and disclosure requirements.

Before Regulation F, the FDCPA didn't directly address digital outreach. That gap created inconsistency across the industry. Now, every SMS and email sent to a debtor must include a clear opt-out mechanism, and collectors must honor those requests promptly, typically within 3 business days.

For businesses working with a debt collection attorney, Regulation F also outlines how legal demand letters and litigation-related communications must be handled. Any attorney-signed communication that misrepresents the collector's intent to sue can expose your business to FDCPA liability, which carries statutory damages of up to $1,000 per violation, plus attorney fees.

What Has Changed in Federal FDCPA Oversight in 2026?

In 2026, CFPB enforcement priorities have shifted toward three main areas: electronic communication abuse, third-party data sharing, and AI-generated contact attempts. Collectors using automated SMS or email campaigns must now document that each message complied with the call and contact frequency limits. The CFPB has increased civil penalty amounts, with knowing violations now carrying penalties up to $50,000 per day under the Consumer Financial Protection Act.

Collectors and creditors using AI-generated messaging are also drawing extra scrutiny. The CFPB released updated supervisory guidance in late 2025 clarifying that AI-drafted communications are subject to the same FDCPA standards as human-written ones. If your vendor uses generative AI to produce collection letters or outreach scripts, those materials must be reviewed by a compliance officer before deployment.

One often-overlooked update: collectors must now retain records of all electronic communications for a minimum of 3 years. That includes SMS logs, email threads, and any platform-generated audit trails.

How Does Florida's FCCPA Affect Your Collections Program?

Florida's Consumer Collection Practices Act (FCCPA) applies to both debt collectors and original creditors, which makes it broader than the federal FDCPA. The FCCPA prohibits communicating with a debtor at their place of employment if the collector knows the employer prohibits such contact. It also bans any conduct that harasses, abuses, or oppresses a debtor.

Most businesses in Central Florida don't realize that the FCCPA allows consumers to sue for actual damages, statutory damages up to $1,000, and attorney fees, all per individual violation. A single misstep in a high-volume collection program can quickly turn into a costly class action.

Local utility providers handling utility collections Florida face a particular challenge here. Regulated utilities in Florida must also comply with Public Service Commission rules that govern disconnect notices and collection timing. For example, residential customers are typically entitled to at least a 5-day written notice before service termination. Missing that window before turning an account over to a collector can create both regulatory and civil exposure.

For businesses operating near Downtown Miami, the Brickell financial district, or even mid-size utility districts serving communities like Doral and Hialeah, these layered requirements demand a clearly documented collections workflow, not just a general familiarity with the rules.

What Are the Risks of Using AI in Your Collections Process?

AI and automation in debt collection raise real compliance concerns that go beyond the technology itself. The core risk is that automated systems, if not properly configured, can exceed the 7-call-per-week cap, generate non-compliant disclosures, or send messages after a consumer has opted out.

The CFPB's 2025 guidance specifically flags "mini-Miranda" warning errors as a top audit finding. Every initial communication with a consumer must include the required disclosure that the communication is from a debt collector and that any information obtained will be used for that purpose. When AI generates these messages, even a small template error can propagate across thousands of accounts before anyone catches it.

For Florida businesses running utility collections, the stakes are even higher. Many utility accounts involve vulnerable customers who are already facing financial hardship. Overly aggressive or technically non-compliant AI-driven outreach can trigger both FCCPA complaints and Public Service Commission reviews.

The safest approach is to treat AI-generated communications as drafts, not final outputs. A licensed compliance professional should review message templates at least quarterly, and any changes to AI system logic should trigger a full compliance review before going live.

What Documentation Do You Need to Minimize Litigation Risk?

Strong documentation is your first line of defense in any FDCPA or FCCPA lawsuit. Courts and regulators look for evidence that your program followed the rules at the time each communication was sent. That means your audit trail needs to capture more than just payment history.

A defensible collections file should include:

- A timestamp and delivery confirmation for every electronic communication

- A record of any opt-out request and the date it was honored

- Call logs showing compliance with the 7-call weekly cap

- Copies of all written disclosures sent to the consumer

- Notes documenting any disputes received and how they were resolved within the required 30-day window

For businesses using third-party collectors or a debt collection attorney network, you also need a signed service agreement that allocates compliance responsibility clearly. If a vendor sends a non-compliant communication on your behalf, your business can still be named in the resulting lawsuit.

We've worked with Florida businesses, including utility providers serving neighborhoods in areas like Coral Gables and North Miami Beach, who discovered after the fact that their vendor's call logs didn't meet the 3-year retention requirement. Getting ahead of that issue before an audit saves significant time and legal fees.

How Do You Build a Compliance Strategy That Holds Up Over Time?

A one-time compliance review isn't enough. Regulation F, FCCPA, and CFPB guidance all evolve, and your program needs to evolve with them. The businesses that avoid costly litigation are those that treat compliance as an ongoing process, not a checkbox.

Start with a written compliance policy that's updated at least once a year. That policy should address contact frequency limits, digital communication procedures, dispute handling timelines, and documentation standards. Assign a specific person or team to own compliance, and give them the authority to pause collection activity when a potential violation is identified.

For utility collections Florida, build a review cycle that accounts for both federal and state rule changes. The CFPB typically issues supervisory updates in the fall, and Florida legislative changes take effect each July 1. Build those dates into your annual compliance calendar.

Train your collections staff, including any third-party vendors, at least twice a year. Document that training. In litigation, evidence that your team received current compliance training can make a significant difference in how a case resolves.

Finally, work with experienced partners. HF Holdings Inc. maintains up-to-date knowledge of FDCPA, Regulation F, and Florida-specific collection rules, and their team handles both standard recovery and escalated legal matters through qualified attorney partners.

Need Help Staying Compliant With Florida Collection Laws?

Regulation F and the FCCPA aren't going away, and CFPB enforcement continues to grow. Whether you manage utility collections Florida, commercial receivables, or consumer accounts, the cost of a compliance gap is far higher than the cost of getting it right the first time.

Contact HF Holdings Inc. at (877) 680-6064 today. Their team can review your current program, identify exposure points, and connect you with the right recovery and legal resources to protect your business going forward.